As investors, we’ve been used to a private fundraising framework that is being completely turned upside down by the public token sale mechanism.

As a venture investor, evaluating investment opportunities is often your full-time job and decisions impact your career as well as your wallet.

As a venture investor you’re also always given access to a lot of detailed confidential material and the access to the team, in order for you to ask questions. And even if in Silicon Valley deals close in record time, and at the seed stage you have to move fast, for Series A+ you have basically as much time as you want to make an investment decision.

Often, as a venture investor you’re also given information rights and sometimes board seats (even thought we’ve recently seen in many companies that in terms of preventing bad behavior these are fairly useless).

In the ICO world, that’s not the case.

Companies, teams or organizations that lunch public token sales, most often never interact with the final token buyer, and the average token buyer has no way to contact the team other than Twitter or their community tool of choice.

On top of that, ICOs are often on extremely tight deadlines, and are surrounded by a lot of hype.

It’s also usually more technically complicated to due diligence such efforts as code is law, and to fully appreciate what’s going on you need to read and understand the smart contracts behind an offering or the code behind a new protocol.

Given that the fundraising efforts are public plus there is little info and little time, I do believe the diligence efforts should be public as well.

When venture investors see deals they don’t like for some reason, or terms that are not fair, they just pass on the deal, and that’s it.

Because other investors will still be full-time investors that will go through the same process of analysis and diligence, and someone might like the deal. (Oftentimes VCs also interact offline about specific deals to get feedback and ask for things they might have missed, especially in advanced diligence).

In a public fundraising deal, even if reserved for accredited investors in the first phase (the token will reach exchanges sometime), investors aren’t usually full-time professional token investors.

Not everyone has time to dig into whitepapers (let alone understand them) and token sale economics to make a very informed judgment.

Yesterday, I did such an effort given no one would write about it. I wrote my sentiment on the token sale economics of Filecoin.

What has surprised me the most, is that aside from a few notes of dissent and criticism, there has been an overwhelming and amazing reaction online.

This post seems to have changed the perception of the token sale for people, which must mean that they did not know the facts presented in the post. This in interesting because those facts were just hiding in plain sight on the token sale documents. In turn, this means that people are very prone to the hype machine but not many have the time to actually go read and ponder about specific token sales.

This is wrong. But to me it should hardly be surprising: I certainly participated in a few token sales where I did not have much information or insight!

I would surely have loved if someone reported on what they found in the docs (and even more importantly the code) for other projects.

I would have loved if Emin Gün Sirer had started the public conversation with The Bancor Protocol before their token sale had started and I’m sure many others would have as well.

Digging into the dynamics of Filecoin’s token sale and economy

Filecoin could be a game changer for the crypto space. It’s one of the few projects that are extremely well thought out, built by an amazing team, and actually needed.

Add to that the fact that they created a new proof mechanism and have a legitimate need for a blockchain.

In other words, it’s probably the best that the crypto community has seen recently. It was certainly one of the few ones I was looking forward to.

Man, I wouldn’t have expected something like this from a solid team. The response felt particularly disingenuous.

I’m now incredibly disappointed, and probably will not participate in the sale.

I’ll also probably lose a good number of friends that are investors in the company and/or pre-sale, but in this new era of completely public fundraising, I think the public deserves to hear it from all sides.

The flaws in Filecoin’s token sale

Filecoin gave an amazing deal to their buddies, just a few weeks ago

Filecoin is being insanely greedy, going out for a $700M+ raise

Early clickers are incentivized, price unknown, network congestion update, see below

Protocol Labs and Filecoin foundation are keeping 2x the coins that investors will get

Problem #1: Filecoin gave an amazing deal to their buddies

There’s nothing that can stop them here, but many people got very mad about this and rightly so.

Filecoin raised $52M in an advisor sale very recently, till July 24th. This sale was reserved for people close to the company and in the industry. Many extremely high profile people participated, total cheques were 150.

These investors paid a maximum of $0.75 per coin. They could also have chosen discounts based on the amount of time the coin would vest, from 0% to 30%.

These investors did not take any more risk than the investors who are going to participate in the public token sale. Actually, one could argue that they even took less risk because they knew what the price would be all the time (which is not going to be the case for public investors)

Their explanation:

All of these people and organizations (a) have been working hard with us for years to make IPFS and Filecoin successful

This is absolutely untrue. Quite a few people just got introduced to the team recently and got into the sale just a week ago and paid the $0.75 price.

(b) have fully committed themselves to work hard with us and for the Filecoin Network for many years to come,

Sure, but you, dear reader, would commit too, wouldn’t you?

c) offer tremendously valuable advice, hands-on help, knowledge, skills, resources, connections, and more.

This is the real reason that they will pay 2x-20x less than you. You be the judge. Usually vested equity is subject to good behavior, but here anyone could promise great advice and help and then disappear, but still get coins.

Problem #2: Filecoin is being insanely greedy

After having raised $52M in a pre-sale for a pre-product offering, they want to go out and raise an amount that is effectively uncapped.

Their response:

Our token sale IS NOT uncapped. It is capped in terms of the amount of Filecoin sold: 200M FIL.

Over the last few years, Protocol Labs has proved to the world that we know how to deploy capital to create valuable projects, valuable technology, and valuable software. To date, all of the work you see — IPFS, libp2p, IPLD, Multiformats, Filecoin, CoinList, and all our research — all our work has been funded by under $3.5M. We know how to deploy capital effectively.

It seems like I’m reading a Trump statement. Basically saying: “I have eaten 10 ice creams in the past years, so I’m great at eating ice creams and can easily eat 1000 in the next few years. Gimme ice creams.”

But aside from the absurdity of trusting someone that deployed $3.5M with $500M+, let’s analyze the USD cap of their token sale.

Some numbers

$52M raised in presale

Minimum 69M, Maximum 99M Filecoins sold in ICO

Advisor max price $0.75

131M-101M Filecoins left for the public

Starting ICO price: $1.3 ($52M/40M), almost 2x advisor price.

Price at $100M raised = $2.5

Price at $200M raised = $5

Unfortunately, their price function is not clear. It doesn’t state if a transaction amount impacts the total raised before calculation of price or after. In any case, assuming normal average investments, eg. $100k, this doesn’t change much.

The USD cap will change based on the average purchase amount and the average discount chosen by the buyers.

Let’s calculate the Filecoin ICO USD cap

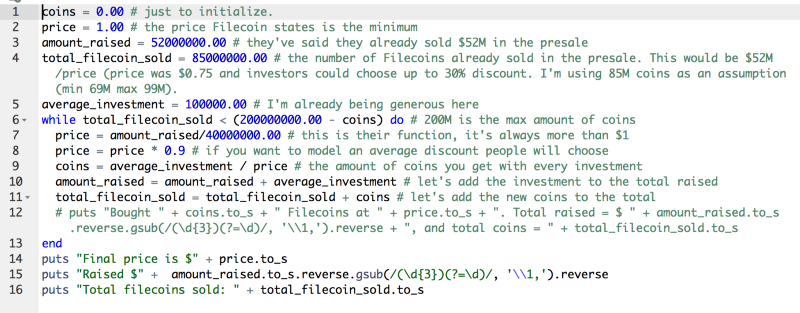

I wrote a small piece of code to calculate the USD raised with different assumptions.

Total Filecoin sold in the advisor pre-sale: 85M (The minimum sold is 69M, if everyone paid $0.75, and the max is 99M, if everyone chose a 30% discount, so I chose something in between)

Average investment = $100,000.00

Average discount chosen by investors: 10% (discounts are 0%, 7.5% for 1y vesting, 15% for 2y vesting, 20% for 3y vesting — I’m assuming many will choose 0 and a few will choose the rest, so 10% sounds about ok.)

The results

Final price is $15.54075 Raised $690,800,000.0 Total filecoins sold: 199999826.3440984

So effectively the cap of Filecoin’s ICO is ~$700M.

For fun, let’s assume no one chooses discounts:

Final price is $34.34 Raised $1,373,700,000.0 Total filecoins sold: 199997793.51623443

The real cap is $1.37B.

And, everyone max discount:

Final price is $7.83 Raised $391,600,000.0 Total filecoins sold: 199991567.59900582

Highly unlikely, but this is the minimum possible cap.

Call me old fashioned, but wanting to raise half a billion dollars for a pre-product endeavor is absolutely fucking insane.

Let’s remember that the tokens will also come out when the network is launched, which Protocol Labs is estimating at 1 year out. Vesting will only start then.

Problem #3: Early clickers are incentivized, price unknown

Given the price grows as more money is invested, early clickers are incentivized to get in as fast as possible — this has the obvious intention of raising as much money as possible.

Users paying in BTC and ETH will also have to wait for their transactions to confirm before knowing how much they paid. Given a very likely clogging of the network, this has the potential for disaster.

I suggest reading their explanation in the response. It is a mix of funny and scary.

Update: rules have changed. Price will be averaged in the first hour and max price in the first hour is $6.

This means that no one will pay the $1.31 min price and buyers in the first hour won’t know how much they’ll pay in the $1.31-$6 bracket.

When the first hour is over, that’s when people will want to fast click because they’ll have information about the price and total raise.

This update just makes it so that there won’t be any price difference for first hour clickers, which is good, but not great. Price is still unknown (and crazy high compared to advisors).

Problem #4: Protocol Labs and Filecoin foundation are keeping 2x the coins that investors will get

This is absolutely mind-boggling to me.

To compare, the ETH genesis sale gave 10% of ETH minted to early contributors and 10% to the Ethereum foundation. 80% was for investors.

In Filecoin’s case, Protocol Labs will receive all the cash PLUS 50% more coins than investors, so 1.5x. A foundation will receive 50% of the amount of coins “minted” by investors. Total: 66.6% to them, 33.3% to you.

Assuming a “small” $250M total raise, Protocol Labs and a foundation would receive, $250M cash, plus $250M-$300M (remember, the discounts?) in tokens.

Also, 70% of the tokens that will ever exist will be mined. This means that the investors are only getting access to 10% of the total supply ever.

As a comparison, Ethereum sold 60,108,506.26 ether at genesis, and today there are 93,775,666.

Place your bets accordingly.

…

Quick and dirty utility value calculation

Edit: I’m removing this as apparently it was way off. I’ll try to spend more time, but with token sale in just a few days not sure I’ll be able to, so prefer to just take it off. All other points I still stand by.

Conclusion

Filecoin is why we can’t have nice things.

A real game changing project, that has always touted they care about the community and would do this for free, is going out trying to raise $700M and keeping double that in coins.

I think this could be one that will be remembered and written in history books about how insane this all was, and how a major innovation like the cryptographic token was taken advantage by people wanting to raise stupid sums of money, before it was really used to the best of its potential.

Thanks to redacted, redacted, redacted, redacted, and redacted for providing feedback on this draft, the ideas behind it, the code and the assumptions for the utility value.